About Us

The Canadian Physicians’ Pension Plan (CPPP) is a federation of individualized pension plans established by professional corporations.

This federation is administered by Canadian Physicians’ Pension Plan Corp. a federal corporation whose mandate is to supervise the selected financial institutions and other partners that service the retirement needs of participating physicians.

CPPP services physicians and their families across Canada in both English and French.

Frequently Asked Questions

How does CPPP work?

The CPPP is a federation of individual pension plans (IPPs or PPPs) set up by the medical professional corporations of physicians. By pooling assets with a single portfolio management firm each physician is able to command lower fees and economies of scale enabling the gradual elimination of actuarial fees over time.

Who is eligible?

Any physician in Canada receiving T4 income (Salary or bonus) from his or her Medical Professional Corporation, if under age 71.

How do I contribute?

The Medical Professional Corporation contributes to the pension plan based on a few factors such as: age of the physician & level of T4 income paid in the current year.

What is the formula to determine benefits?

The defined benefit provided by the plan is generated by the following formula:

2% x Pensionable Salary x Years of Credited Service.

Example: If the Salary is $100,000 and the Physician contributes for 30 years, the annual pension paid in retirement would be:

= 2% x 100,000 x 30

= $2,000 x 30

= $60,000/year

Retirement, defined

Retirement under CPPP simply means no longer receiving T4 income/salary from the Medical Professional Corporation and turning on the annual promised pension. A physician can continue to practice medicine and Provincial Health Systems will pay the Professional Corporation for services rendered. At that point, the Physician can receive both a regular pension from CPPP and dividends from the Medical Professional Corporation.

What would happen if I took a leave of absence?

Presumably, the Physician may decide to stop receiving a salary from the Medical Professional Corporation (“MPC”). Since tax deductible contributions made by the MPC are a percentage of T4 income paid, the contributions would stop during the leave of absence. The plan would continue to exist until the physician comes back into active participation or decides to retire instead.

How is my family protected after my passing?

In two main ways. If family members also participate in the plan because they receive T4 remuneration as well, upon the death of the Physician member, the retirement capital inside the plan is not taxed and this surplus remains available for the survivors to enjoy.

If family members do not participate in the plan, they can still appear as “designated beneficiaries” of the Plan. Upon the death of the physician, in the absence of a surviving spouse, the assets of the pension plan are paid to the designated beneficiaries.

What Canadian provinces is CPPP available?

Physicians across Canada can join CPPP.

Are there investment management fees?

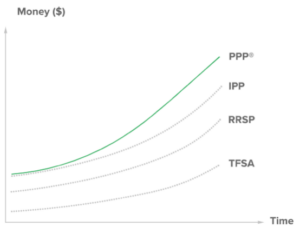

Yes, the portfolio manager that invests the assets of CPPP customers levies investment management fees calculated by reference to total assets under management. These fees are fully tax deductible to the Medical Professional Corporation. Moreover, because the pension plan offers 6 new additional contributions beyond those offered by RRSPs, the tax savings and additional assets available for retirement cover these fees multiple times over.

What kind of ROI can I expect by participating in CPPP?

While the ultimate Return on Investment varies depending on the risk appetite of the physician, the balanced approach followed by CPPP’s portfolio manager aims for a consistent return between 6% to 10%, with minimal risk of loss of capital invested.

Is it possible to recover or fund pension contributions for prior years through the CRA under a CPPP structure? If yes, how does the process work?

- Yes, if a Medical Professional Corporation (MPC) paid a physician T4 income in previous years, since the CPPP is a collection of registered pension plans (RPPs) under RPP rules, a purchase of past service is possible.

- The process is that we calculate the years of past service being purchased and indicate how much of that cost comes from existing RRSPs or RRSP room and how much comes from the MPC itself.

- Contributions made by the MPC are tax-deductible.

Am I required to increase my salary annually to maintain or optimize CPPP contributions?

There is no legal obligation to increase the salary, but since the total level of tax deductions is a percentage of Salary/T4, never increasing the salary means that some extra contribution room is lost every year, since CRA updates the limits upwards.

Do required or recommended pension contributions increase each year? What determines that increase?

Actuarial science is the basis for the increasing percentage of salary that forms the annual contribution to the pension plan.

Can previously accumulated RRSP funds be transferred into the CPPP?

Yes and furthermore such transfer is tax-sheltered. Moreover, once RRSP funds are transferred to the CPPP, a number of additional advantages are triggered such as:

a) all Investment Management Fees that were non-deductible when assets sat in an RRSP now become tax deductible to the MPC

b) better creditor protection

c) access to non-RRSP eligible investments (e.g. direct private real estate)

d) potentially better treatment in the case of death thanks to section 56 of the Income Tax Act that makes the taxation occur in the hands of the beneficiaries instead of in the Estate of the RRSP holder. This opens up the potential for significant income splitting across multiple tax returns.

If I currently have unused RRSP contribution room, can that room be converted or utilized within the CPPP?

Yes. Functionally that is what will happen if we recognize past service.

If I do not have sufficient cash available to make contributions upfront, can contributions be made after receiving tax refunds or reimbursements from CRA? Or how does it done?

It is important to note that contributions are never mandatory under CPPP and carry forward to the next years (until the next valuation). If the only source of cash that the MPC / Employer has to contribute to the CPPP are tax refunds / reimbursements, then it is only at that time that the MPC will be in a position to contribute.

What are the main risks or downsides of a CPPP?

If someone sets up a pension plan under CPPP but then never uses it and never contributes to it, all of the advantages are neutralized (except perhaps creditor protection on any funds transferred and fee deductions) and there is an ongoing annual cost that still needs to be paid. Much like buying a Time Share in Florida and never finding time to go and use the properties displayed because one is too busy.

Does concentrating retirement savings in this structure create diversification concerns?

Should not because the portfolio of the CPPP is extremely diversified in its own right and can be further diversified by the portfolio manager if the Physician client/members wishes to do so.

To what extent can a CPPP reduce corporate tax?

Every case depends on its own facts, but generally speaking we can triple or quadruple the tax deductions otherwise available to an individual physician. Therefore whereas an RRSP might give a physician a $30,000 deduction to reduce taxes, the CPPP could provide $120,000 in deductions instead, relying on the multiple tax deductions available under pension laws: (i) past service (ii) higher annual current service (iii) RRSP double dip (iv) pension adjustment offset amount (v) special payments (vi) investment management fee deductions (vii) interest deductions (viii) terminal funding.

Is it realistic for it to reduce corporate tax payable close to zero?

Depends but usually not every single year. It is not outside of the realm of possibilities for a Pension Plan to give an MPC a $1,000,000 corporate tax deduction under the “Terminal Funding” rules. If OHIP only paid the MPC $1 000,000 in billings that particular year, the pension plan could reduce the corporate tax payable to zero. But you can only do Terminal Funding once. Where the tax deductions of the CPPP are insufficient, we recommend layering a supplemental pension plan called the Retirement Compensation Arrangement (RCA). It comes with its own tax deductions and those can usually be well beyond those permitted by the CPPP rules.

What investment flexibility exists within a CPPP?

Extremely wide. But Canadian securities laws don’t allow for “self-directed” pension investing, as is the case with RRSPs.

How does this compare to an Individual Pension Plan (IPP) in terms of choosing investment assets?

No difference, both the IPP and CPPP follow the exact same investment legislation.

How can you help my accountant in formulating tax papers as he is against the PPP?

Yes, we have a lot of information we can share with Accountants. Note that if the CPA is against PPPs, but fine with IPPs, we can set up an IPP instead.

What’s the difference between PPP and CPPP and IPP?

CPPP is an umbrella, or federation of IPPs and PPPs that individual MPCs have set up for their individual shareholder physicians. Being a Group provides for economies of scale and a reduction of the annual administrative fees. An IPP is a defined benefit only pension plan. A PPP is a combination pension plan that offers both the ability to build up a pension using the Defined Benefit rules (i.e. IPP) or alternatively by using Defined Contribution rules.

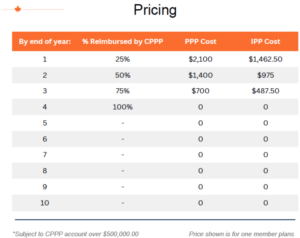

What are the fees involved in setting up?

We don’t charge set up fees.

There is an annual administration fee (1950$ for IPP, $2800 for PPP) but that fee is progressively discounted to 0,00 $ by the end of year 3 if assets under management exceed $500,000.

Do you charge fee to coordinate with personal accountant?

No.

How much can I contribute?

Depends on many factors but usually significantly more than under an RRSP.

Can I contribute into a RRSP while contributing into the PPP?

Yes in the first year and very limited ($600) in subsequent years.

Can I choose my own portfolio of investment in PPP or it has to be through your company?

If you are simply doing an IPP or PPP with INTEGRIS you can select your own portfolio manager. If you choose CPPP, the portfolio manager is communal to all members but there is some flexibility as to how your individual pension assets are to be invested.

How much will you charge for managing the portfolio?

CPPP currently runs at 1.2% on assets (lower for very large accounts).

What if I decided to use my own investment online platform instead?

Self Directed investing is not permitted in Canada for pension plans only for RRSPs and other types of accounts.

If my children are part of the pension plan, but no longer works for my Corp, do they still have access to my plan’s money?

Yes, we would make sure they are qualified as ‘deferred vested members’ meaning that upon your demise they would have the surplus left behind even though they are no longer employed by your MPC.

Can PPP be contributed into life insurance?

Yes.

How is the RRSP affected when I contribute to the pension plan?

We need to report Pension Adjustments every year to the CRA and the CRA uses that information to reduce the RRSP room normally generated by receiving ‘earned income’.

Is it too late to contribute to a pension plan if you plan to work for another 10 years?

No. Contributions and deductions granted to the MPC can continue even past 71, something that RRSPs cannot offer.